Insurance

In addition to helping our clients understand how true wealth works, our firm also specializes in crafting health, life, and disability income protection solutions for individuals and business.

Health Insurance

All plans available are ACA approved. To get a customized health insurance quote, and see if you qualify for a subsidized plan, see the BlueCross BlueShield® information below

Click the button below to go to Blue Cross Blue Shield and get a quote, enroll or find the plan that fits your situation. If you have any questions don’t hesitate to contact Joe.

Life Insurance

Times have changed. The way many Americans view their finances today has shifted dramatically over the past few years. Today, individuals are looking to take less financial risk than ever before. Consequently, a growing number of consumers are rediscovering a financial product that has been available for years— Whole Life insurance.

Whole Life insurance

The main purpose of Whole Life insurance is to provide valuable guaranteed financial protection whenever the insured should die. But what many do not realize is that it’s so much more. Whole Life provides a wide array of financial benefits, including “living benefits” — a term that refers to the fact that a Whole Life policy provides a ready source of funds for any purpose throughout the policyowner’s lifetime or during key income-producing years.

The main purpose of Whole Life insurance is to provide valuable guaranteed financial protection whenever the insured should die. But what many do not realize is that it’s so much more. Whole Life provides a wide array of financial benefits, including “living benefits” — a term that refers to the fact that a Whole Life policy provides a ready source of funds for any purpose throughout the policyowner’s lifetime or during key income-producing years.

For many years, some financial experts have attempted to discredit Whole Life insurance— while promoting the supposed benefits of other insurance policies that, in certain market environments seemed to offer higher returns at lower costs.

But what we’ve learned in recent years is that some policies ultimately required some policyowners to pay additional premiums in order to keep their policy in force.

For many, the “recovery” cost was beyond reach. The good news is that doesn’t happen with Whole Life.

Life insurance is an intangible. It’s not like a car or an item of clothing. While life insurance can provide a good deal of protection and long-term financial secclie policy beneficiaries, the intangible nature of this product leads many life insurance consumers to pursue what they feel is a “better deal” when considering their lifelong insurance needs. But it’s important for those same individuals to understand these “truths” with respect to their pursuit of a better deal.

Truth #1 Life insurance policy illustrations—especially many UL and VUL policies—portray an attractively impossible outcome

Policy illustrations often quote a low price (planned premium) that often can’t be sustained over the life of the policy

Illustrations of non-guaranteed policies can conceal the likelihood that the illustrated planned premium will turn out to be insufficient when:

- calculated with current expenses and returns projected decades into the future

- the insurer has the right to increase its internal pricing structure; and

- the interest or investment return factors are assumed to remain the same (which, in reality, they never do).

Even the disclaimer required by insurance regulators on every policy illustration warns of the limited usefulness of the illustration data: “illustration [results] are neither a projection nor a guarantee of future results.”

The way to better portray a probable outcome is to use a policy that is guaranteed. Whole Life has valuable guarantees built in. These guaranteed rates and values can help create a more consistent and reliable projection than a policy without guarantees. And these guarantees provide balance to other (non-insurance) portions of your portfolio in which you are taking risk.

Truth #2 We can’t reasonably answer the question: “Which policy will perform better?”

- If there is one thing that we know about the economy, it’s that it is always changing. That has created some major repercussions over the years for life insurance policyowners who own policies that didn’t have guaranteed premiums.

- Illustrations calculating “premiums” for universal life in 1982 with 14 percent crediting rates created an unrealizable long-term expectation that couldn’t be supported as interest rates plunged in today’s low levels. As a result, most policies issued in the early 1980s that are still in force are paying only the rate guaranteed in the policy (which is invariably higher that the rate used for policies issued today).

- Illustrations calculating variable universal life premiums in 1997 with the regulated maximum illustration rate of 12 percent also created an unrealizable expectation as investment returns plunged in early 2000 and again in 2008-2009. These changing conditions required the policyowner to pay additional premiums—sometimes at much higher levels than those originally illustrated—in order to avoid having the policy lapse during the insured’s lifetime.

- Although historical performance can’t be used to predict the future, it can give you some important insights into what type of unpredictable volatility you can expect with policies that don’t have guaranteed premiums. If volatility is a problem—consider Whole Life.

Truth #3 There’s a cliché that says, “If it’s too good to be true, it probably is.”

- Potential buyers often focus too much on the “attractive impossibility” presented by the illustration—without understanding what is required in order to keep an insurance policy in force over the insured’s lifetime.

- In truth, the focus should be on the agent and insurance company—not the product. A worthwhile relationship between a financial services company and an agent starts with your goals and objectives, moves on to your available cash flow or assets, and presents suitable products from financially strong companies that relate to your own situation in a prudent and realistic way.

- It’s important for consumers to be careful of how and what they are being sold. Because the right life insurance is meant to last a lifetime.

Truth #4 Start with an asset allocation instead of a set interest rate.

- Interest rates in the U.S. have risen and fallen frequently over the last 40 years—and will continue to do so in the future.

- Investment returns have been very volatile in the last 20 years and are likely to remain so. Because lower returns can cause a policy’s cost of insurance to increase, the effect of interest rate and investment return volatility cannot be overlooked.

- For example, the 40-year compound return on investments in the period from 1/1/1968 to 12/31/2007 yielded a return 200 basis points (2.00%) higher than investing in the period one year later from 1/1/1969 to 12/31/2008!

- Many times a client’s asset allocation for investments is similar to their allocation for their life insurance, although many prefer a more conservative approach for their insurance.

- Guarantees found in Whole Life insurance create a conservative asset that is similar to other fixed income assets in a portfolio.

Truth #5 Everyone loves a good deal—that’s human nature.

- But: There is no free lunch. The sweet taste of an apparent bargain pales in comparison to the bitter experience of bad quality. Think how many times you thoughtyou got a bargain, but got a dog instead.

- Most of us have bought enough items that seemed like a “good deal”—but turned out to be something entirely different in the end.

- There are things that can—and should—be pursued on the basis of lowest price. But life insurance isn’t one of them, since the longevity of the policy is put at risk if the premiums paid are insufficient to sustain the policy over the long term.

- The good news, when talking about most permanent life insurance, is that the full premium is not a sunk cost—you get value back today and tomorrow.

- While you should address price with your insurance professional for your individual situation, be sure to also focus on value. There is value in putting more money into a tax-advantaged vehicle like life insurance. In addition to the potential tax savings, it can also lead to higher cash values and longer guaranteed coverage within your policy—giving your life insurance strategy the potential for a higher rate of success.

Understanding the truths we’ve explored here can help you assess your needs and make more objective and informed decisions about the life insurance you purchase—for the long-term protection of your loved ones.

Still Financial, LLC, its agents, or employees do not give tax or legal advice. You should consult your tax or legal advisor regarding your individual situation.

Disability Insurance

Why Do You Need Disability Insurance?

But what if illness or injury made it impossible for you to work?

- How long would your savings last?

- Would your spouse’s or partner’s income be sufficient to make up the shortfall?

- What lifestyle changes would you or your family need to make?

- What about your dreams for the future— College for your children, travel, a comfortable retirement?

- What would happen to your credit rating?

Are There Alternatives?

It’s really important to think through each possible “Plan B”. However, are any of these really viable alternatives?

Personal Assets: Most financial advisors recommend counting on cash reserves only for the first few months. A long-term disability can rapidly erode assets.

Social Security: Given the stringent requirements to qualify for benefits, fewer than 30% of claims are approved at the initial level. After all appeals, only about half of claims are ultimately approved. (Source: Social Security Administration, 2006)

Workers Compensation Benefits generally cover employees for job-related accidents and illness, not those suffered outside of the workplace.

State Temporary Disability: NY, NJ, CA, HI, and RI provide a minimal level of short-term coverage for employees. Other states offer no such coverage.

Group LTD: Employer and association long-term disability plans are highly variable, but rarely offer benefits like a guaranteed premium or cost of living adjustment. Benefits under employer plans are generally offset by Social Security and other government programs. Review your coverage carefully.

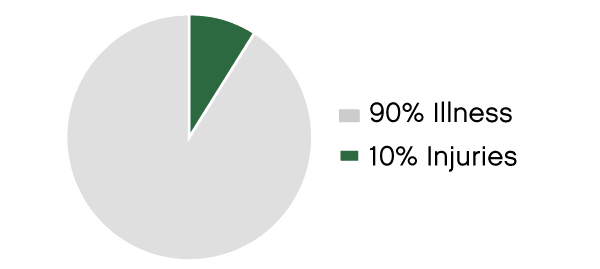

What Causes Most Disabilities?

Musculoskeletal/connective tissue ……………………………27.5%

Cancer …………………………………………………………..14.6%

Cardiovascular …………………………………………………9.1 %

Maternity-related ………………………………………………5.1%

Injuries/accidents ………………………………………………10.3%

Mental/psychiatric disorder………………………………………9.1 %

Neurological ………………………………………………………6.9%

Source: 2011 Long-Term Disability Claims Review, Council for Disability Awareness. For more information go to www.disabilitycanhappen.org.

Policy Benefit Examples

*Non-Cancellable and Guaranteed Renewable An insurance company cannot cancel your policy, increase your premiums or change policy provisions if you keep paying premiums due, until a certain age (normally age 65). After that, you can renew your policy at rates then in effect as long as you continue to be gainfully employed full time.

Total Disability You will be considered totally disabled if, solely due to injury or sickness, you are not able to perform the material and substantial duties of your occupation, even if you are gainfully employed in another occupation.

Your occupation means the occupation(s) in which you are gainfully employed during the 12 months prior to the time you became disabled.

If you have limited your occupation to the performance of the material and substantial duties of a single medical or dental specialty, that will be deemed your occupation.

Waiver of Premium Any premiums that are due while you are disabled and receiving benefits will be waived, and for 6 months after you recover. Also, any portion of premium you have paid that applies to the period after you first became disabled will be refunded.

Occupational Rehabilitation, Modification and Access Benefits The insured may be eligible for an occupational rehabilitation benefit that is part of a mutually agreed-upon formal plan. Additionally, the insured may be eligible for a reimbursement benefit for the cost of workplace modifications that will help the insured return to gainful employment.

Elimination Period The elimination period is the number of days that must elapse before benefits become payable. You may be disabled from the same or a different cause for this entire period. Days of disability need not be consecutive, but must occur within an accumulation period of 210 days.

Waiver of Elimination Period The elimination period can be waived if you become totally disabled within five years after the end of a previous disability that lasted more than 6 months and for which you have received benefits.

Benefit Period This is the longest period of time for which an insurance company will pay benefits for a continuous disability from the same cause.

Recurrent Disability If, after a disability for which you have been paid benefits, you return to full-time gainful employment but become disabled again within 12 months, the later period of disability will be considered a continuation of the previous one. The later period of disability must result from the same cause or causes as the previous disability. Benefits will resume with no new elimination period required.

Presumptive Disability An insurance company will consider you totally disabled—even if you are gainfully employed—if you suffer total and complete loss of sight in both eyes; hearing in both ears; speech; or the use of both hands, both feet, or one hand and one foot, in their entirety. Your loss does not have to be irrecoverable.

Capital Sum Benefit An additional lump sum benefit is payable for specified losses: total loss of sight in one eye, or loss of a hand or foot. This benefit equals 12 times your monthly indemnity.

for more info check out the Guardian® brochure “Short Course in Individual Disability Insurance”